A Cup of JOE (7/16)

No Need to Be Alarmed by Job Openings Yet

Marissa Hashizume, NLx Research Hub Economist

July 16, 2026

Welcome to A Cup of JOE, a blog series. Each post will serve up fresh insights into U.S. job openings using the NLx Job Opening Estimator (NLx JOE) — a tool that blends federal government data with NLx Research Hub data and analytics to provide timely, detailed estimates of labor demand trends. Whether you’re a workforce professional, researcher, or just curious about employment opportunities, this series will keep you informed on interesting and emerging trends in labor demand, supporting data-driven decision-making and broader awareness of what is happening in the labor market.

We’re still in a relatively calm phase for the labor market overall (“low hire, low fire”) and that includes job openings. Job openings were just slightly lower in Q2 this year than they were in Q2 last year (7.3M vs. 7.4M). Monthly job openings have been gently declining in the past few months (7.5M estimated in March, 7.3M in June) following a dip and subsequent rebound between November and March. Remember that these are not seasonally adjusted estimates, so some of these changes could merely be seasonality, although seasonal fluctuations tend to be less pronounced than bigger trends in our estimates.

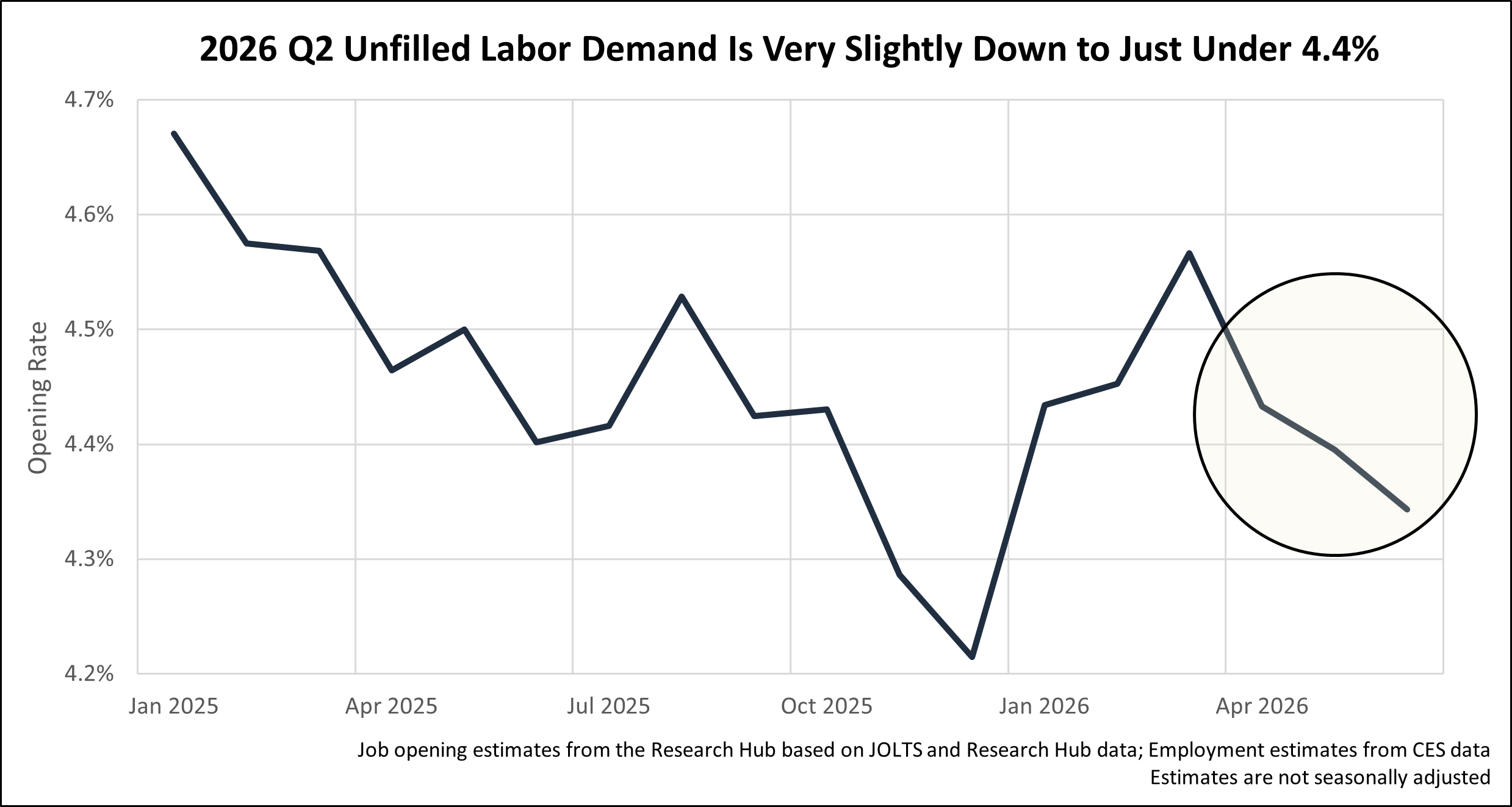

Looking at job openings as a portion of all labor demand (unfilled labor demand), we see similar patterns. There is a lot in the news about employment changes (going up by a lot and then not a lot), but the magnitude of those changes is very tiny in the scheme of employment overall (hundreds of thousands vs. hundreds of millions). In other words, employment fluctuations have been minimal, so unfilled labor demand patterns are very similar to the pattern in job openings: slightly lower in Q2 (4.39% of labor demand unfilled) than Q1 (4.48%) of this year or Q2 of last year (4.46%) but nothing alarming.

Labor market tightness, measured by the number of openings per unemployed person, has now been consistently hovering around the balance point (one opening per one unemployed person) for the past year. While we again had a slight decline over the course of Q2 this year (1.09 in April, 0.97 in June), that was mostly due to the seasonality of unemployment fluctuations (not seasonally adjusted) which are typically low in April and peak in July (don’t worry, seasonally adjusted employment is still generally trending down). While removing seasonal fluctuations is helpful for identifying larger trends and measuring broader economic health, the not seasonally adjusted measures are more closely related to how people are actually experiencing the labor market. So, very generally speaking, it might be slightly harder for workers to find a job now than a few months ago or easier for employers to find workers (slight loosening) but is similar to this time last year.

Note that unemployment data is unavailable for Oct. 2025 due to the government shutdown. We have filled in the missing unemployment data with the average of Sep. and Nov. unemployment to avoid a gap. Please see this BLS announcement for more information on the impact of the shutdown on the CPS statistics, including higher standard errors for Nov. 2025.

More broadly, the U.S. labor market has done fairly well in the face of recent external shocks. The Boston Fed published a piece on how our economy has changed since the 1970s in ways that have allowed for smaller direct employment impacts from negative oil shocks. However, there is still potential for indirect impacts, for example, via higher inflation, which could affect how employers and workers navigate the labor market. There are also other uncertainties playing out domestically and abroad that have potential implications for the labor market in the second half of this year.

***A Cup of JOE examines job opening estimates from the NLx Job Opening Estimator (NLx JOE). Explore job opening numbers, see methodology notes, and more on NLx JOE, updated with new estimates monthly. Note that estimates from the most recent months are subject to minor revisions after additional federal data becomes available.***